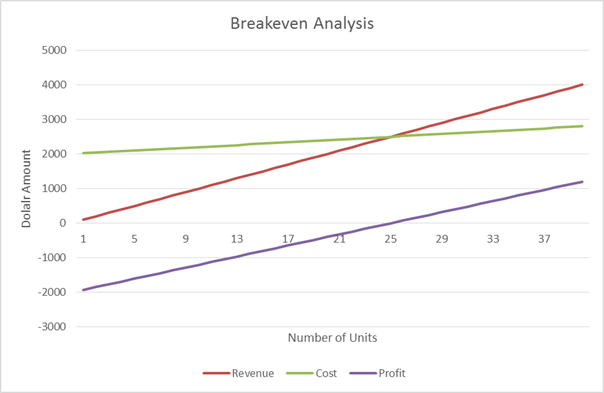

Breakeven Analysis is used to calculate the number of units you need to sell in order to cover all of your fixed and variable costs.

Equation

Break Even Analysis:

Fixed Costs / (Price per Unit – Cost per Unit) = Quantity to Produce

Quantity to Produce (Price per Unit – Cost per Unit) – Fixed Cost = Amount Earned

Example

- Item A is sold for $100 per unit.

- Item A costs $20 per unit

- Company X has fixed costs of $2,000

The breakeven point is:

$2,000 / ($100 – $20) = 25 units